Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Choosing the Right Mortgage Term: 15-Year Fixed vs. 30-Year Fixed Mortgage

Buying a home is one of the most significant financial decisions you’ll ever make. When it comes to financing your dream home, the choice between a 15-year fixed mortgage and a 30-year fixed mortgage can have a lasting impact on your financial future. In this guide, we’ll break down the differences between these two popular mortgage options, helping you navigate the complexities and make an informed decision that aligns with your goals.

Understanding the Basics:

A 15-year fixed mortgage and a 30-year fixed mortgage are two primary options for financing your home purchase. The terms refer to the length of time over which you’ll repay the loan. Let’s explore the key distinctions between these two choices:

1. Loan Term:

– **15-Year Fixed Mortgage:** As the name suggests, this mortgage option comes with a 15-year loan term. You’ll make payments for 15 years to fully repay the loan.

– **30-Year Fixed Mortgage:** With a 30-year mortgage, your loan term spans three decades.

2. Monthly Payments:

– **15-Year Fixed Mortgage:** Monthly payments are higher due to the shorter repayment period. This can impact your budget and affordability.

– **30-Year Fixed Mortgage:** Monthly payments are lower compared to a 15-year mortgage, offering greater flexibility in managing your finances.

3. Interest Rates:

– **15-Year Fixed Mortgage:** Typically comes with lower interest rates compared to a 30-year mortgage, leading to substantial interest savings over time.

– **30-Year Fixed Mortgage:** Interest rates are often slightly higher due to the extended repayment period.

4. Interest Paid:

– **15-Year Fixed Mortgage:** You’ll pay significantly less in total interest over the life of the loan.

– **30-Year Fixed Mortgage:** Due to the longer term, you’ll end up paying more in total interest.

5. Equity Buildup:

– **15-Year Fixed Mortgage:** Equity in your home builds up faster because of the shorter repayment schedule.

– **30-Year Fixed Mortgage:** Equity accumulates more slowly as a larger portion of early payments goes toward interest.

PROS AND CONS:

**15-Year Fixed Mortgage:**

– Pros: Faster loan payoff, lower overall interest payments, quicker equity buildup, potentially lower interest rates.

– Cons: Higher monthly payments, potential strain on budget, lower loan amount eligibility.

**30-Year Fixed Mortgage:**

– Pros: Lower monthly payments, greater flexibility in budgeting, potentially higher loan amount eligibility.

– Cons: Higher total interest paid, slower equity buildup.

Making Your Decision:

When deciding between these two mortgage options, consider your financial situation, goals, and risk tolerance. If you can comfortably afford higher monthly payments and want to save on interest in the long run, a 15-year mortgage might be ideal. On the other hand, if you prefer lower monthly payments and more financial flexibility, a 30-year mortgage could suit you better.

Use mortgage calculators to compare scenarios and understand how different terms impact payments and interest. Additionally, consult a financial advisor or mortgage professional to receive personalized advice tailored to your circumstances.

Remember, the choice between a 15-year fixed mortgage and a 30-year fixed mortgage isn’t just about the loan term. It affects interest rates, monthly payments, total interest paid, and equity buildup. By carefully weighing these factors, you’ll be well-equipped to choose the mortgage option that aligns with your current and long-term financial goals.

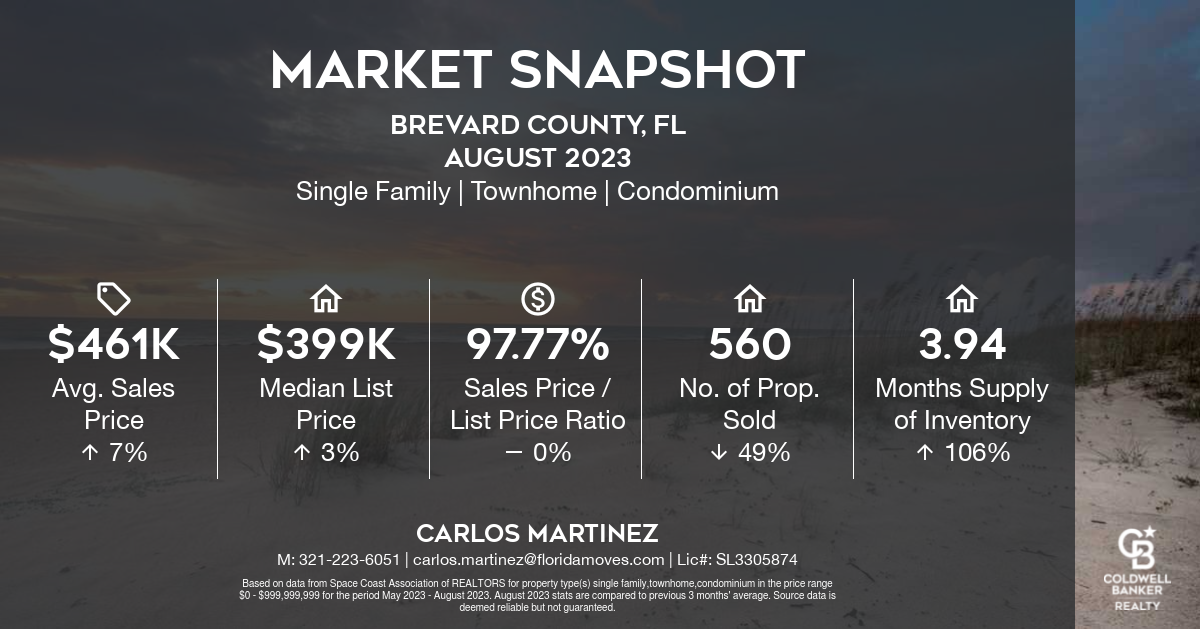

Market Snapshot for August 2023

**Exploring the Vibrant Real Estate Market of Brevard County, Florida – August 2023 Update**

As the summer heat continues to embrace the picturesque landscapes of Brevard County, Florida, the local real estate market is sizzling as well. In this month’s update, we delve into the latest trends and statistics for single-family homes, townhomes, and condominiums. The numbers paint a promising picture, indicating robust growth and a dynamic market that’s attracting both buyers and sellers alike.

**Average Sales Price Soars to $461,000 with a 7% Increase**

One of the most significant highlights of the August 2023 Brevard County real estate market update is the remarkable increase in the average sales price for residential properties. As of this month, the average sales price has reached an impressive $461,000, reflecting an impressive 7% surge. This surge signifies the area’s desirability and the strong demand for housing options across the county.

**Median List Price Climbs to $399,000 with a 3% Increase**

For those considering selling their homes or investment properties, the market conditions are undoubtedly favorable. The median list price in August 2023 stands at $399,000, marking a commendable 3%. This upward trend speaks volumes about the confidence sellers have in the current market’s stability and potential for profit.

**Sales Price List Price Ratio at 97.77% – A Balanced Market for Buyers and Sellers**

The Brevard County real estate market has maintained a healthy balance between buyers and sellers, evident from the Sales Price List Price Ratio of 97.77%. This ratio showcases the equilibrium between the initial listing price of properties and the final selling price they command. Both parties can negotiate and transact with confidence, knowing that fair deals are being struck.

**Robust Sales Activity: 560 Properties Sold**

The momentum of the Brevard County real estate market is palpable, with a total of 560 properties successfully changing hands in the month of August. This robust sales activity further demonstrates the resilience and popularity of the county as a sought-after destination for both residents and investors.

**Inventory Levels and Months of Inventory**

For those keeping a close eye on market trends, the inventory levels and months of inventory provide crucial insights. As of August 2023, the market has maintained a balanced supply-demand ratio, with a comfortable 3.94 months of inventory available. This means that at the current sales pace, it would take approximately 3.94 months to deplete the available inventory, striking a harmonious balance between supply and demand.

In conclusion, the Brevard County real estate market continues to shine in August 2023, with impressive price growth, healthy sales activity, and balanced market conditions. Whether you’re a potential buyer, seller, or investor, the current trends indicate a dynamic environment that welcomes various opportunities. As the summer sun sets over the Atlantic coast, the Brevard County real estate market remains illuminated by the promise of a thriving and prosperous future.

Sellers: Don’t Let this hold you back

Many homeowners thinking about selling have two key things holding them back. That’s feeling locked in by today’s higher mortgage rates and worrying they won’t be able to find something to buy while supply is so low. Let’s dive into each challenge and give you some helpful advice on how to overcome these obstacles.

Challenge #1: The Reluctance to Take on a Higher Mortgage Rate

According to the Federal Housing Finance Agency (FHFA), the average interest rate for current homeowners with mortgages is less than 4%.

But today, the typical 30-year fixed mortgage rate offered to buyers is closer to 7%. As a result, many homeowners are opting to stay put instead of moving to another home with a higher borrowing cost. This is a situation known as the mortgage rate lock-in effect.

The Advice: Waiting May Not Pay Off

While experts project mortgage rates will gradually fall this year as inflation cools, that doesn’t necessarily mean you should wait to sell. Mortgage rates are notoriously hard to predict. And, right now home prices are back on the rise. If you move now, you’ll at least beat rising home prices when you buy your next home. And, if experts are right and rates fall, you can always refinance later if that happens.

Challenge #2: The Fear of Not Finding Something to Buy

When so many homeowners are reluctant to take on a higher rate, fewer homes are going to come onto the market. That’s going to keep inventory low. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

Even though you know this limited housing supply helps your house stand out to eager buyers, it may also make you feel hesitant to sell because you don’t want to struggle to find something to purchase.

The Advice: Broaden Your Search

If fear you won’t be able to find your next home is the primary thing holding you back, remember to consider all your options. Looking at all housing types including condos, townhouses, and even newly built houses can help give you more to choose from. Plus, if you’re able to work fully remote or hybrid, you may be able to consider areas you hadn’t previously searched. If you can look further from your place of work, you may have more affordable options.

Bottom Line

Instead of focusing on the challenges, focus on what you can control. Let’s connect so you’re working with a professional who has the experience to navigate these waters and find the perfect home for you.

The Power of Preapproval: Unlocking Home Buying Sucess

The Power of Preapproval: Unlocking Home Buying Success

Searching for your dream home can be an exciting and rewarding journey, but it’s essential to approach it with a solid plan in mind. One crucial step that often gets overlooked is getting preapproved for a mortgage before you start house hunting. In this blog, we’ll explore why obtaining a preapproval is a wise move for home buyers and the significant benefits it brings to your home buying experience.

1. What is a Preapproval?

Before we dive into the benefits, let’s quickly clarify what a preapproval entails. A preapproval is a process in which a mortgage lender reviews your financial information and determines the amount they are willing to lend you for purchasing a home. It’s important to note that a preapproval is not the same as a prequalification, as it carries more weight and requires more documentation.

2. Increased Buying Power:

One of the most significant advantages of obtaining a preapproval is the increase in your buying power. By having a preapproval letter in hand, you’ll know precisely how much you can afford and can confidently explore homes within your budget. This knowledge helps you narrow down your options and saves you time by focusing on properties that align with your financial capacity.

3. Competitive Edge:

In a competitive real estate market, where multiple buyers may be eyeing for the same property, a preapproval can give you a significant edge. Sellers are more likely to take your offer seriously if you are preapproved, as it demonstrates that you are a serious and reliable buyer. In some cases, sellers may even prioritize preapproved offers over others, potentially giving you an advantage in negotiations.

4. Faster Closing Process:

When you’re preapproved for a mortgage, the lender has already assessed your financial situation and determined your eligibility. This means that once you find the perfect home, the mortgage approval process can move swiftly. With a preapproval, you can avoid delays and expedite the closing process, ensuring a smoother and more efficient transaction.

5. Budgeting and Financial Planning:

Obtaining a preapproval helps you create a more accurate budget for your home purchase. By knowing the loan amount you qualify for, you can calculate your monthly mortgage payments and estimate the additional costs associated with homeownership, such as property taxes and insurance. This information allows you to plan your finances better and avoid any surprises down the road.

6. Confidence and Peace of Mind:

Lastly, getting preapproved provides you with confidence and peace of mind throughout the home buying process. You can confidently make offers on properties within your budget, knowing that your financing is in order. Additionally, having a preapproval in hand can alleviate stress and uncertainty, allowing you to focus on finding the perfect home without worrying about your financial eligibility.

Conclusion:

While it may seem tempting to jump straight into house hunting, taking the time to get preapproved for a mortgage is a smart move that brings numerous benefits. From increased buying power and a competitive edge to a faster closing process and improved financial planning, preapproval sets you up for success in your home buying journey. So, before you start browsing listings, make sure to connect with a reputable lender and get preapproved. You’ll be glad you did!

Remember, your dream home awaits, and preapproval is the key to unlocking its door.

Call me for your Real Estate needs Carlos Martinez 321-223-6051 Carlossellsdreamhomes.com

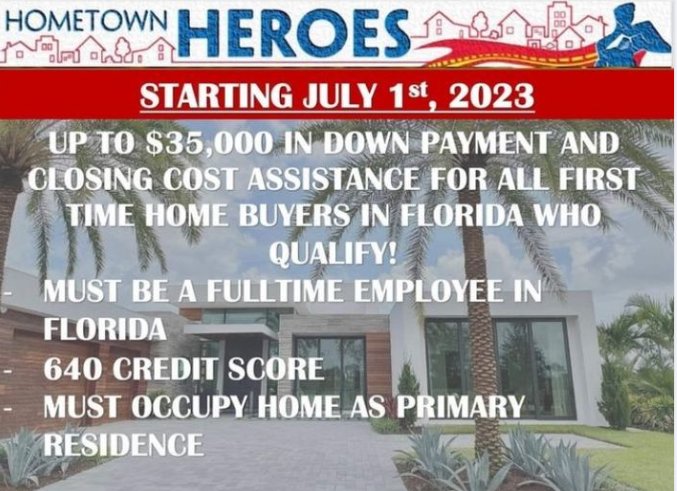

HOMETOWN HEROES FIRST TIME BUYER PROGRAM

🌟 Attention, Florida Community! Introducing the Florida Hometown Heroes Housing Program! 🏡🎉

Hey there, wonderful friends! I have some incredible news to share with you today that will make homeownership more affordable for eligible members of our community. 🌟 It’s called the Florida Hometown Heroes Housing Program, and it’s designed to support our hardworking workforce in achieving their dreams of owning a home.

This program provides down payment and closing cost assistance to first-time, income-qualified homebuyers who live and serve in our community. 🦸♀️🦸♂️ It’s our way of giving back to those who work tirelessly to make our hometown a better place.

Let’s dive into some important program details that you need to know:

1️⃣ Lower Interest Rates: Eligible full-time workforce employed by a Florida-based employer can benefit from lower than market interest rates on FHA, VA, RD, Fannie Mae, or Freddie Mac first mortgages. This means you can enjoy more affordable monthly payments and save money in the long run.

2️⃣ Down Payment and Closing Cost Assistance: We understand that saving for a down payment and covering closing costs can be a challenge. That’s why this program offers up to 5% of the first mortgage loan amount (maximum of $35,000) in down payment and closing cost assistance. This financial boost can help make your homeownership dreams a reality.

3️⃣ Deferred Second Mortgage: The down payment and closing cost assistance is provided in the form of a 0%, non-amortizing, 30-year deferred second mortgage. It’s important to note that this second mortgage becomes due and payable, in full, upon the sale of the property, refinancing of the first mortgage, transfer of deed, or if the homeowner no longer occupies the property as their primary residence. It’s designed to help you now while ensuring the program remains sustainable for future homebuyers.

4️⃣ Additional Benefits for Service Members: For those who have served or continue to serve our country, the Florida Hometown Heroes Loan Program offers even more special benefits. These benefits can further enhance your homebuying experience and make it even more affordable and rewarding.

Don’t miss out on this amazing opportunity to make your homeownership dreams come true. Take advantage of the Florida Hometown Heroes Housing Program and start building a brighter future for yourself and your family.

If you or someone you know is eligible and ready to take the next step towards homeownership, don’t hesitate to reach out. Tag your friends, share this post, and spread the word about this incredible program!

#FloridaHometownHeroes #AffordableHomeownership #CommunityWorkforce #MakingDreamsComeTrue #SupportingOurHeroes

The Long-Term Value of Homeownership Despite High Interest Rates

In today’s economic climate, high interest rates have become a topic of concern for prospective homeowners. While it’s true that rising interest rates can impact mortgage affordability, homeownership still remains a financially sound decision with numerous long-term benefits. In this blog post, we will explore why homeownership is the right path to take, even in the face of high interest rates.

1. Stability and Control:

One of the primary advantages of homeownership is the stability it offers. When you own a home, you gain a sense of control over your living situation, as you are no longer at the mercy of fluctuating rental costs or the whims of landlords. High interest rates may raise the cost of borrowing, but the stability and control that come with owning a home provide peace of mind and a solid foundation for the future.

2. Building Equity:

One of the most significant long-term benefits of homeownership is the opportunity to build equity. Each mortgage payment made reduces the outstanding loan balance, thereby increasing your ownership stake in the property. Over time, as property values appreciate, you can potentially build substantial equity. This equity can then be leveraged for future financial needs, such as renovations, education expenses, or even as a source of retirement income.

3. Tax Advantages:

Homeownership offers several tax advantages that can help offset the impact of high interest rates. Mortgage interest and property tax payments are typically tax-deductible, reducing your overall tax liability. Additionally, if you decide to sell your home in the future, you may be eligible for capital gains tax exemptions (subject to certain conditions). These tax benefits can have a significant positive impact on your overall financial situation.

4. Potential for Appreciation:

Despite short-term fluctuations, real estate has historically proven to be a valuable long-term investment. High interest rates may slightly dampen the immediate appreciation potential, but over time, as the housing market stabilizes, property values tend to increase. By investing in a home now, you position yourself to benefit from future appreciation, allowing you to grow your wealth steadily.

5. Rent Savings:

When considering the impact of high interest rates, it’s important to compare homeownership costs with the alternative of renting. While rising interest rates may make homeownership seem less affordable, renting often comes with its own set of challenges. Rent payments can increase annually, and you don’t have the advantage of building equity or enjoying potential tax deductions. Over time, homeownership tends to be more cost-effective, as you are investing in an asset that can appreciate in value.

Conclusion:

High interest rates may give potential homeowners pause, but it’s important to look at the bigger picture. Homeownership offers stability, control, and the opportunity to build equity, even in the face of temporary challenges. The tax advantages and potential for long-term appreciation further enhance the financial benefits of homeownership. Rather than focusing solely on short-term interest rate fluctuations, consider the long-term value and security that owning a home can provide. By making informed decisions, you can navigate the current market conditions and embark on a rewarding journey towards homeownership.

TOP 10 BENEFITS OF BUYING VS RENTING

TOP 10 BENEFITS OF BUYING A HOME INSTEAD OF RENTING:

- Equity Building: One of the key advantages of buying a property is that it allows you to build equity over time. Instead of paying rent and essentially contributing to someone else’s wealth, your mortgage payments go towards owning an asset that can appreciate in value.

- Long-Term Investment: Buying a home is often seen as a long-term investment. Over time, real estate has historically appreciated in value, providing homeowners with the potential for financial growth. This can be beneficial when you decide to sell the property in the future.

- Stability and Security: When you own a home, you have a sense of stability and security that renting may not provide. You have control over your living space, the freedom to make modifications, and the comfort of knowing that you have a place to call your own.

- Tax Benefits: Homeownership often comes with certain tax advantages. Mortgage interest and property tax payments may be tax-deductible, reducing your overall tax liability and potentially providing additional financial savings.

- Customization and Personalization: Unlike rental properties, homeownership gives you the freedom to personalize and customize your living space to suit your preferences. You can paint the walls, renovate the kitchen, or make any other changes that make the home truly yours.

- Sense of Community: Buying a home often means becoming part of a community. You have the opportunity to establish roots, build relationships with neighbors, and engage in local activities. This sense of community can contribute to your overall quality of life.

- Potential Rental Income: If you decide to move out of your home in the future, you may have the option to rent it out and generate passive income. This can be a valuable source of additional revenue or even help cover the mortgage payments on your new property.

- No Landlord Restrictions: Homeownership frees you from the limitations and restrictions often imposed by landlords. You have more control over your living arrangements, such as having pets, making modifications, or adjusting the property to suit your specific needs.

- Pride of Ownership: Owning a home brings a sense of pride and accomplishment. It allows you to establish roots, create memories, and build a place that truly reflects your personality and style.

- Long-Term Cost Savings: While the upfront costs of buying a home can be higher than renting, homeownership can provide long-term cost savings. As you pay off your mortgage, you eliminate the monthly payment and have the potential to build wealth through property appreciation.